Join Us in Dallas, ‘Simplifying Together’ Formation ’24

Formation brings together thought-leaders and the top P&C and general insurance carriers from around the globe for a dynamic in-person industry event.

Built for Insurers

Evolve and Innovate Faster With

Duck Creek’s Full Suite of Insurance Technology

Humanize Experiences

Build trust and deliver more empathetic and personalized customer experiences.

Faster Speed-to-Market

Capture ever-changing P&C insurance needs with low-code tools and reusable product modules.

Grow Distribution Channels

Increase sales and enhance agent and broker loyalty and satisfaction.

Customer Success Stories

“We chose Duck Creek because of the low-code configurability of the system. That’s something that’s very important to us. The developers are able to quickly implement changes without changing code.”

Blair Sturts

Senior Vice President Information Technology,

Cumberland Mutual

What’s New at Duck Creek

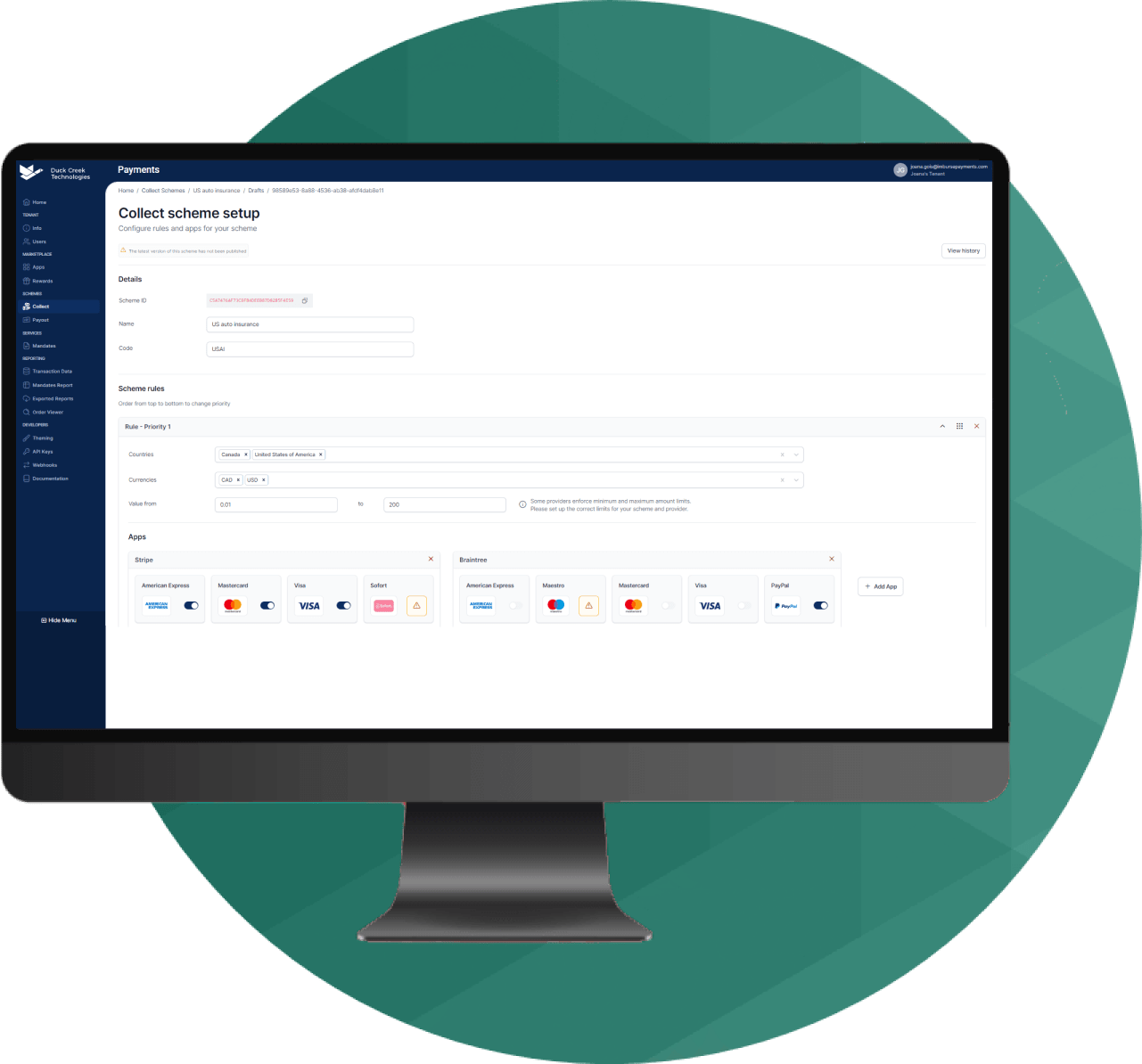

Duck Creek Payments

Connect to the entire global payments ecosystem for collections and payouts regardless of existing IT infrastructure and finance process.

Our Trusted Partnerships

We are proud to partner with leading technology innovators worldwide, empowering insurers to define their future success.

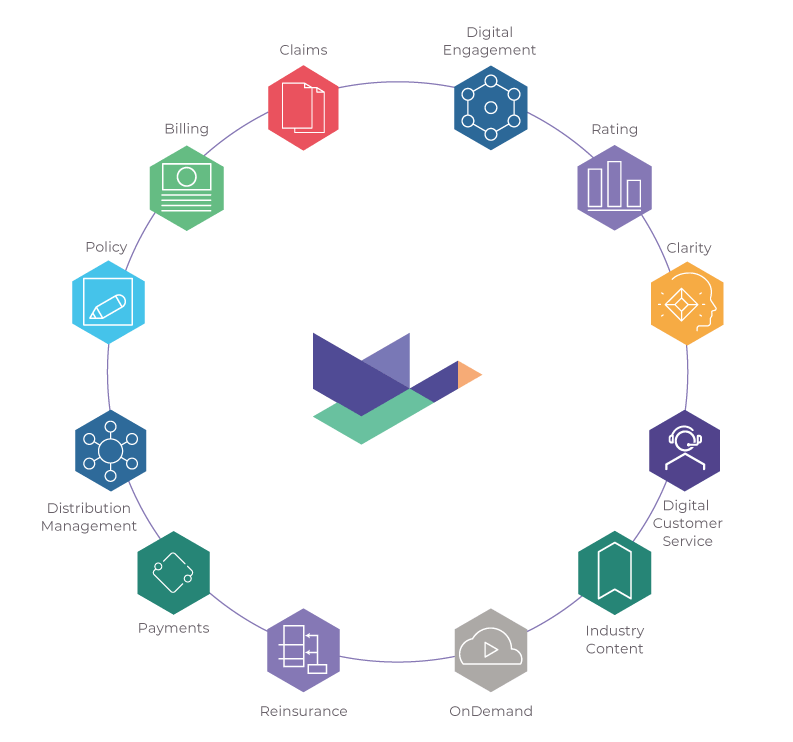

End-to-End

Insurance Capabilities

There’s something for every step of the insurance lifecycle. Simplify complexity with Duck Creek’s modern, intelligent, and humanized technology.

- 200+ customers and 1,100+ successful implementations

- 50,000+ transactions for policies processed daily

- 30 million+ claims processed in the cloud

- 130+ partner integrations and 2,600+ APIs across all Duck Creek applications

Create P&C Insurance Products Faster Than Ever

The age of personalized and humanized insurance means that P&C insurers worldwide are expected to rapidly develop and deploy new insurance products and update existing ones whenever consumer needs arise.

Find out how Duck Creek enables insurers to create and scale new products at speed.

Talk to Sales Today

The only way to see if Duck Creek is the right fit for your P&C insurance business is to see it in action. Let us show you how Duck Creek can make your business goals a reality.